Why, how and when multi-asset investors should rebalance

In this article, we discuss why, how and when multi-asset investors might consider rebalancing their portfolios, as well as common techniques

In this article, we discuss why, how and when multi-asset investors might consider rebalancing their portfolios, as well as common techniques

Understanding the various strategies and techniques that can be used to manage and maintain a multi-asset portfolio can help advisers guide clients towards investment success. Rebalancing is one such strategy, and its importance cannot be overstated, because it can help clients achieve their long-term financial goals by managing risk throughout their investment journey.

In this article, we discuss why, how and when multi-asset investors might consider rebalancing their portfolios, as well as common techniques for doing so.

In essence, rebalancing is the process of adjusting a portfolio’s mix of assets based on a predetermined or updated target asset allocation.

For asset allocation strategies where the target mix of equities and bonds is fixed, portfolio rebalancing entails selling the best-performing securities in a portfolio over a given time period and using the proceeds to invest in the poorer-performing securities, with a view to maintaining the desired mix of equities and bonds in the portfolio.

While this might seem counterintuitive to some clients, the practice can help reduce portfolio volatility, avoid portfolio ‘drift’ and ultimately help investors stick to their long-term investment strategy. That’s because without systematically rebalancing, portfolio allocations can drift from their intended long-term target as the returns of constituent assets diverge, leading to much higher portfolio risk.

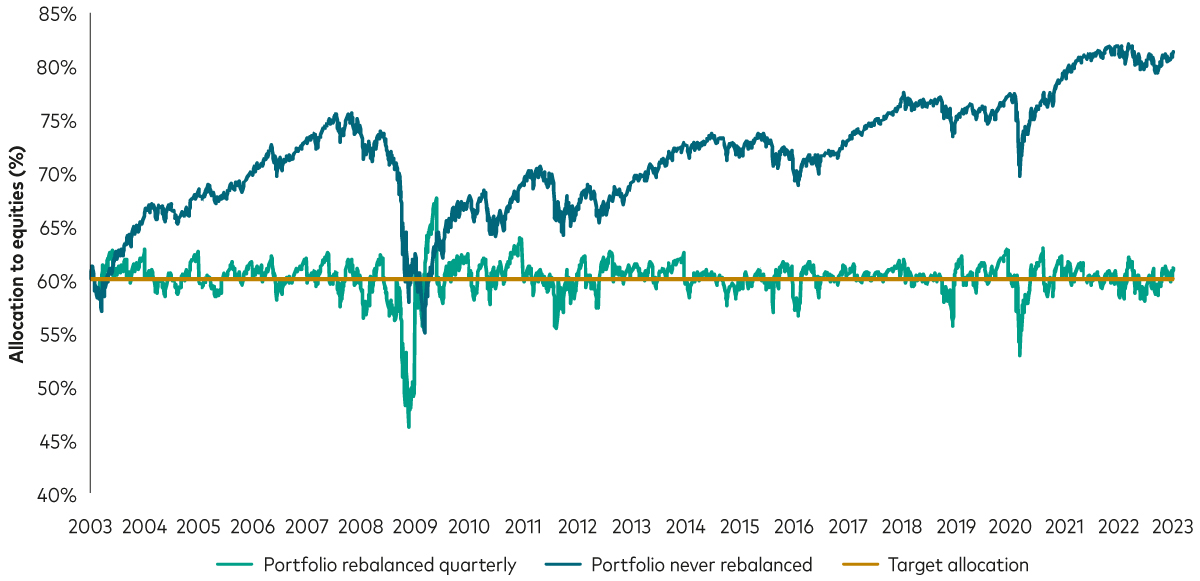

For example, a portfolio with an asset allocation of 60% global equities and 40% global bonds at the end of 2003, if never rebalanced, would have had 80% in equities at the end of 2022, as shown in the chart below. In contrast, an identical portfolio that was rebalanced at the end of each quarter would have maintained the target allocation and the desired risk profile over time.

Changes in stock exposure for a 60/40 rebalanced portfolio and a "drifting portfolio"

Past performance is not a reliable indicator of future results

Sources: Vanguard, using data from Bloomberg. Notes: Daily returns data from 1 January 2003 to 10 February 2022. The initial allocation for both portfolios is 42% US stocks, 18% international stocks, and 40% US bonds. The rebalanced portfolio is returned to this allocation at the start of each quarter. Returns for the US stock allocation are based on the Dow Jones US Total Stock Market Index until 1 April 2005 and on the MSCI US Broad Market Index thereafter. Returns for the international stock allocation are based on the MSCI All Country World Index ex USA and returns for the bond allocation are based on the Bloomberg US Aggregate Bond Index. All returns calculated in USD.

By allowing a portfolio to drift, clients may find their portfolios are more sensitive to stock market downturns, or equally could be left holding a portfolio that is no longer in line with their investment aims. This is where regular rebalancing can make a difference by keeping investors on track to meet their investment objectives.

Before we examine rebalancing strategies, it’s important to note that the primary function of portfolio rebalancing in the example outlined above is to keep a client’s investments aligned with their tolerance for risk – not to maximise returns.

But rebalancing can also be used with the intention of improving returns. In the case of time-varying asset allocation (or dynamic) strategies, rebalancing can also refer to the process of reviewing and adjusting the target mix of assets based on the latest medium-term forecasts. In this instance, portfolio rebalancing is intended to optimise portfolio returns according to a specific or broad investment objective, such as an annual return target or risk threshold.

The rebalanced portfolio in the chart above uses a simple time-only rebalancing strategy. Such a strategy rebalances on a given date, regardless of the relative performance of the portfolio’s component assets. But other approaches are available to advisers. For example, with a threshold-only strategy, rebalancing is triggered when a portfolio’s asset allocation has drifted by a given amount, say by five percentage points, irrespective of how often this happens.

A strategy combining a time and threshold approach will monitor the portfolio on a given schedule and have pre-set thresholds, but rebalancing will only occur when the two trigger-points intersect. Here’s a simple breakdown of three common approaches to rebalancing:

Rebalancing on a set schedule, such as daily, monthly, quarterly or annually.

Rebalancing when a target asset allocation deviates by a predetermined number of percentage points, such as 1%, 5% or 10%.

Rebalancing on a set schedule, but only if a target asset allocation deviates by a predetermined amount of percentage points, such as 1%, 5% or 10%.

Each approach has its own pros and cons based on individual circumstances, meaning advisers may want to research each technique thoroughly before selecting which one works best for each clients. Additionally, common pitfalls, such as chasing returns or taking too much risk, should be avoided when trying to rebalance portfolios.

Different rebalancing strategies may be better suited for different types of clients, portfolios and markets. For example, periodic rebalancing may be more beneficial for investors with larger portfolios compared with those with smaller ones, who may prefer trigger-based rebalancing strategies instead. By understanding these various strategies, advisers can tailor the approach to individual clients. Alternatively, multi-asset managers often provide an automatic rebalancing service on behalf of advisers as part of their multi-asset offering. For example, Vanguard’s LifeStrategy funds rebalance on a daily basis to ensure that the target asset allocation is maintained.

Much research has been commissioned to attempt to identify the optimal rebalancing strategy, with mixed results. Vanguard’s latest research analysed the efficiency of annual, quarterly and monthly rebalancing strategies based on simulated market returns using our proprietary forecasting tool, the Vanguard Capital Markets Model (VCMM). The analysis considered cost-efficiency, portfolio volatility and post-transaction wealth as part of each approach’s overall efficiency.

During periods of heightened market volatility, less frequent portfolio rebalancing, i.e., annually, was found to be more efficient than quarterly or monthly approaches. That’s because transaction costs tend to rise during volatile environments1, which makes rebalancing more costly. Moreover, an investor may rebalance in one direction and then have to reverse the transaction because the market swung sharply the opposite way, which can happen during periods of turmoil.

Broadly speaking, the analysis found that the optimal rebalancing method is one that is neither too frequent, such as monthly or quarterly calendar-based methods, nor too infrequent, such as rebalancing only every two years. But a more frequent approach, such as daily rebalancing, can also help clients achieve investment success, provided it is implemented in a consistent and cost-effective way.

The responsibility is ultimately on advisers to identify the most appropriate rebalancing approach for clients and apply it in a consistent and disciplined manner to give them the best chance of reaching their long-term financial goals. There are certain actions and considerations that Vanguard recommends to maximise rebalancing efficiency, including:

Cash inflows, such as lump-sum investments, dividends and interest, should be directed into underweighted asset classes. Cash outflows, such as withdrawals from the portfolio, should start with overweighted asset classes.

Rebalancing only partially towards your target allocation can limit transaction costs. However, if the portfolio has drifted a long way from its target allocation, a partial rebalancing may still leave the portfolio with a substantially different risk profile to its target.

By rebalancing within tax-advantaged accounts first, advisers can reduce the tax burden of rebalancing across the client’s entire portfolio.

Vanguard’s multi-asset funds and model portfolios are regularly rebalanced by our in-house investment teams in a disciplined and cost-effective way that is appropriate for each strategy, giving advisers more time back to focus on other value-add tasks, such as behavioural coaching, for example.

Rebalancing is an important component for successful multi-asset investing and ensures client portfolios remain within the desired risk profile over time.

There are several ways advisers can implement rebalancing, including time-only, threshold-only and time and threshold.

Being mindful of costs, taxes and cash flows can assist in making the rebalancing process as efficient as possible.

1 Vanguard calculations, based on data from FactSet. Notes: Analysis of actual and predicted bid-ask spread of securities within the S&P 500 between 1 January 2016 and 30 June 2020. See Y. Zhang, H. Ahluwalia, A. Ying, M. Rabinovich and A. Geysen, 2022 “Rational rebalancing: An analytical approach to multi-asset portfolio rebalancing decisions and insights.”

If you have completed all content in the module, you are ready to take the quiz and collect your CPD

Ready to test your knowledge?

Take the quizCPD content designed to help you build your practice, market your services effectively and cultivate a thriving professional network.

CPD content crafted to empower you to service your client’s needs effectively, build relationships, create loyalty and achieve new business growth.

CPD content structured to give you access to useful tools, guides and multimedia resources covering diverse topics from risk profiling to retirement planning.

Investment risk information

The value of investments, and the income from them, may fall or rise and investors may get back less than they invested.

Important information

This article is designed for use by, and is directed only at persons resident in the UK.

The information contained in this article is not to be regarded as an offer to buy or sell or the solicitation of any offer to buy or sell securities in any jurisdiction where such an offer or solicitation is against the law, or to anyone to whom it is unlawful to make such an offer or solicitation, or if the person making the offer or solicitation is not qualified to do so. The information in this document does not constitute legal, tax, or investment advice. You must not, therefore, rely on the content of this article when making any investment decisions.

The information contained in this article is for educational purposes only and is not a recommendation or solicitation to buy or sell investments.

© 2025 Vanguard Asset Management, Limited. All rights reserved.

Vanguard Asset Management, Limited is authorised and regulated in the UK by the Financial Conduct Authority.