Why inflation expectations matter

Many market participants have been saying the recent jump in inflation is transitory. Inflation spikes can seem transitory, though, until they aren’t.

As outlined in Vanguard global chief economist Joe Davis’s recent blog, we don’t envisage a return to the stagflationary environment—characterised by stagnant economic activity amid high unemployment and inflation—of the 1970s. But are we nearing the point where rises in price levels evolve to become a more permanent structural shift in inflation trends? We considered this question in a recent research paper, The Inflation Machine: How It Works and Where It’s Going.

While most economists, including those in Vanguard’s Investment Strategy Group, believe that the current spike we’re seeing in inflation will prove transitory, our research shows that actual inflation is highly responsive to changes in inflation expectations. There is risk that higher inflation could bleed into expectations, and that could trigger a self-fulfilling prophecy and lead to higher future inflation.

Linking inflation expectations to actual inflation

Inflation expectations reflect how much businesses and consumers expect prices to rise (or fall) in the future. Expectations tend to be “well anchored”, meaning they don’t fluctuate much in response to actual incoming inflation data.

Changing circumstances, however, can lead businesses to expect their costs to rise significantly in the future. When that happens, businesses may raise the prices of their goods and services to cover the expected rise in their costs, which then feeds into actual inflation. Similarly, workers may look for pay increases to cover an anticipated acceleration in the cost of living; those wage increases would also show up in higher actual inflation down the road.

Central banks play a key role in keeping inflation expectations anchored. Since taming runaway inflation four decades ago, the US Federal Reserve (Fed) has earned a reputation for its ability and willingness to use monetary policy to combat price instability. That credibility informs the relationship between expectations and inflation in our model. Any change in that credibility—for example, markets and consumers seeing the Fed as slow to react to incipient inflation—could change the relationship between expectations and realised inflation, threatening to dislodge anchored expectations more easily than in the past.

Quantifying the link

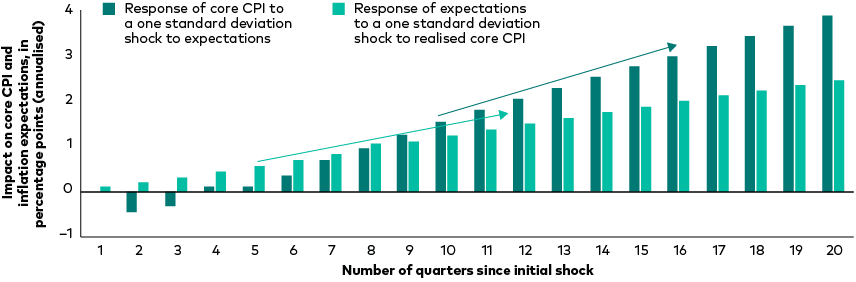

Our research shows that there is a feedback loop whereby changes in inflation affect inflation expectations and vice versa, albeit not to the same extent.

We looked specifically at the relationship between inflation, as measured by the core Consumer Price Index (CPI), and inflation expectations, as measured by an adaptive/recursive measure of inflation expectations based on the core CPI, to see how a movement of one standard deviation in one of these variables affects the other over time.

The chart below illustrates one of our findings: While the relationship extends in both directions, the impact on actual inflation from a change in inflation expectations (shown by the dark green arrow) is greater than the impact on inflation expectations from a change in actual inflation (shown by the flatter slope of the light green arrow).

Actual inflation is more responsive to a change in inflation expectations than the other way around

Notes: The bars represent the impact on inflation expectations (light green) and core CPI (dark green) from a one standard deviation shock to the other variable. The impacts are derived from the impulse response functions in Vanguard’s inflation machine model.

Sources: Estimates using data from Thomson Reuters Datastream, U.S. Bureau of Economic Analysis and Moody’s Data Buffet, based on Vanguard’s inflation machine model.

Why inflation expectations matter now

A key takeaway from our inflation forecast model is that the current consensus is too sanguine about inflation settling into its pre-pandemic trend of 2% in 2022. Factors that could keep inflation above that level include solid but protracted labour market gains, strong economic growth, continued fiscal spending and rising inflation expectations.

Expectations are especially important in the current environment. Recent actual inflation readings have been coming in at levels not seen in decades. The consensus is that price increases will soon cool, but the longer today’s inflationary spike lasts, the greater the risk that expectations become dislodged, which could raise the medium- and long-term inflation outlook.

Investment risk information

The value of investments, and the income from them, may fall or rise and investors may get back less than they invested.

Any projections should be regarded as hypothetical in nature and do not reflect or guarantee future results.

Important information

For professional investors only (as defined under the MiFID II Directive) investing for their own account (including management companies (fund of funds) and professional clients investing on behalf of their discretionary clients). In Switzerland for professional investors only. Not to be distributed to the public.

The information contained in this document is not to be regarded as an offer to buy or sell or the solicitation of any offer to buy or sell securities in any jurisdiction where such an offer or solicitation is against the law, or to anyone to whom it is unlawful to make such an offer or solicitation, or if the person making the offer or solicitation is not qualified to do so. The information in this document does not constitute legal, tax, or investment advice. You must not, therefore, rely on the content of this document when making any investment decisions.

Issued in EEA by Vanguard Group (Ireland) Limited which is regulated in Ireland by the Central Bank of Ireland.

Issued in Switzerland by Vanguard Investments Switzerland GmbH.

Issued by Vanguard Asset Management, Limited which is authorised and regulated in the UK by the Financial Conduct Authority.

© 2021 Vanguard Group (Ireland) Limited. All rights reserved.

© 2021 Vanguard Investments Switzerland GmbH. All rights reserved.

© 2021 Vanguard Asset Management, Limited. All rights reserved.

923