A consistent approach to active fixed income

Commentary by Nick Eisinger, emerging markets lead strategist, and Sarang Kulkarni, portfolio manager, investment-grade credit.

For most investors, fixed income should be the part of their portfolio they can rely on – the solid bedrock that delivers stability, in good times and bad. The importance of consistency applies as much to active fixed income as it does to bond index exposures, as achieving consistent returns or alpha with active bond funds is pivotal to helping investors and their clients meet their long-term objectives.

But how can active bond fund managers generate alpha from asset classes like global credit or emerging market bonds that investors can rely on?

Diversified sources of alpha

In our view, consistent, risk-adjusted alpha generation is at the heart of what makes a good active bond fund. As such, when expressing an active view, we think of the risk of the trade, and the strategy, first.

At Vanguard, one of the key ways we achieve this is with a security selection-focused strategy built on diversified sources of alpha. Rather than relying on concentrated or correlated risk positions to generate returns, our active fixed income teams construct portfolios using strategies with high information ratios – in other words, those opportunities offering the best active returns relative to the risk incurred.

The security selection opportunities we seek can come from a diverse set of origins. For example, our in-house global credit research team, including research analysts and traders, constantly scour their opportunity sets for attractive situations based on forward-looking fundamentals. These range from internally assigned credit ratings to company financials to ESG risk, among others. The analysts can tease out ideas that are long term in nature as well as those that are event- or valuation-driven.

Our security-selection expertise allows us to derive value from even the most stressed credits. For example, in 2020, as the coronavirus crisis hit the travel and leisure sector, our Global Credit Bond Fund took a position in a bond issued by a company in the transportation services sector. While the market did not favour the credit at the time, our team identified fundamental value, and we took a profit the following year, exiting the position after the bond had delivered strong outperformance relative to its benchmark. Patience, prudence and smart risk-taking underline our approach.

Another source of alpha is relative-value opportunities, involving considerations such as credit curve analysis, beta-adjusted forecasts and cross-currency analysis. The close collaboration between our credit researchers and traders also contributes to alpha. Our fixed income traders add value in a number of ways, including through relative value, technicals input and issue-specific analysis. Though fundamentals are critical, appreciating how much an asset is worth is equally important.

Emerging markets are constantly evolving and offer a widely dispersed opportunity set that lends itself particularly well to active decisions, notably with regard to security selection on a relative-value basis. The investment options across credit-quality considerations, issuance in local versus major currencies and sovereigns versus corporates, and many other variables, are huge.

Managing asset class-specific risk

Taking an appropriate approach for each fixed income sub-asset class is critical to best exploiting the opportunities available and delivering consistent alpha. It can also help mitigate asset class-specific risks.

For example, in global credit, in addition to seeking to achieve consistent returns through security selection, we also focus on high-quality, investment-grade holdings that should act as a diversifier relative to equities through varying market conditions. Our global fixed income team with their bottom-up, fundamentals-based insight, combined with our disciplined approach to risk-taking, helps make this possible.

Similarly, in emerging market bonds, we also maintain a broad variety of focused opportunities as part of our risk-controlled process, aiming to avoid the potential for significant drawdowns as well as aiming to provide consistent returns. There is a misconception that emerging market bonds are highly-volatile and risky investments. However, data over 20 years show that volatility in the asset class is lower than in many equity markets with similar levels of return. And it can be the case that emerging market bonds deliver equity-like returns with the level of volatility normally associated with fixed income1.

Even positions in emerging market restructuring situations can add value and mitigate drawdown risk, albeit on a selective basis and at the right price. Managed in an appropriate way, with rigorous fundamental analysis and a robust risk-focused investment approach, investments in distressed sovereigns can make a meaningful positive contribution to emerging market portfolios.

If we have a bias to anything, it is liquidity. Seeking alpha doesn’t mean sacrificing liquidity. Our funds aim to be nimble and consistent without giving up the liquidity profile of our funds.

As a result, our investment teams seek to access the best active opportunities while preserving the risk-dampening qualities of bonds that many investors value.

Alpha, or “levered beta”?

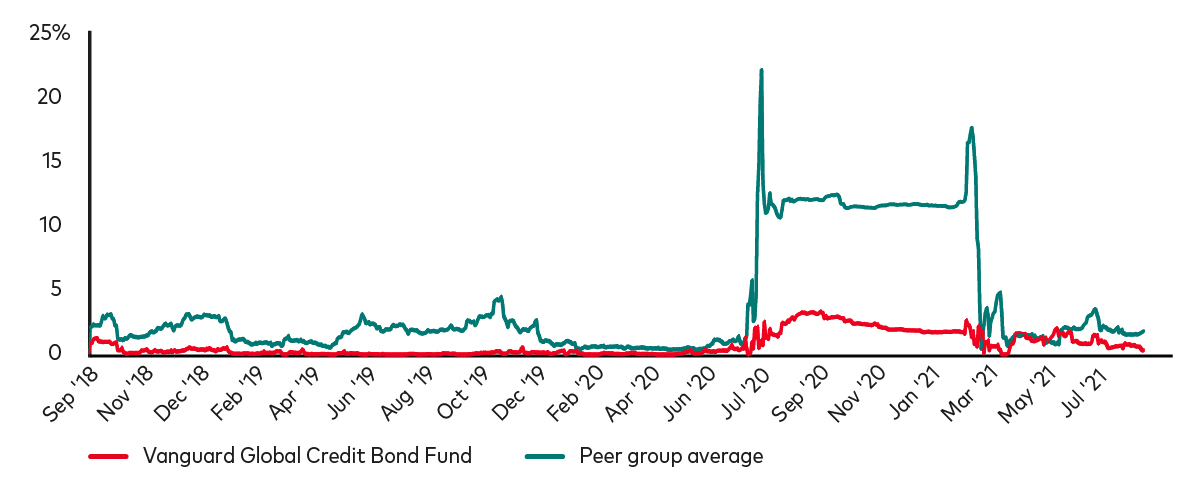

Some active bond funds make use of a strategy that is sometimes referred to as “levered beta” – that is, making excessive bets on the direction of bond markets in an attempt to generate returns. Such strategies might fare well in risk-on scenarios, but can fall down in more volatile environments.

For example, the chart illustrates the proportion of the Vanguard Global Credit Bond Fund’s active risk that is attributable to credit beta relative to the average of other funds in its peer group2 during the highly-volatile coronavirus crisis. While the Vanguard fund’s percentage is consistently below 5% during the period, the competitor average of active risk explained by credit beta exceeded 20% at times.

Percentage of active risk explained by credit beta (rolling one-year)

Source: Morningstar, Bloomberg and Vanguard from 30 September 2018 to 15 January 2021. Peer group defined by Morningstar - EAA OE Global Corporate Bond - USD Hedged.

Dependable fixed income beta does have a key role to play in portfolios, but investors should be clear whether the use of beta is a passive or active decision. Crucially, there is no reason for investors to pay active management fees for a product that derives its returns largely from a passive relationship to beta.

When we use beta in our active funds, it is a conscious decision and only when we deem it beneficial to performance. However, we are deliberate in avoiding unintended beta and the associated levering of unnecessary risk.

When it comes to active fixed income, as with all of our products, we believe that investors should know what they’re investing in.

True-to-label products

Vanguard’s active fixed income funds are all transparent and true-to-label. That means that as well as having the goal of achieving consistent alpha generation over the market cycle, they all have a similar risk and asset-class profile to the assets they represent, allowing the flexibility to add value while staying true to the character of the fund.

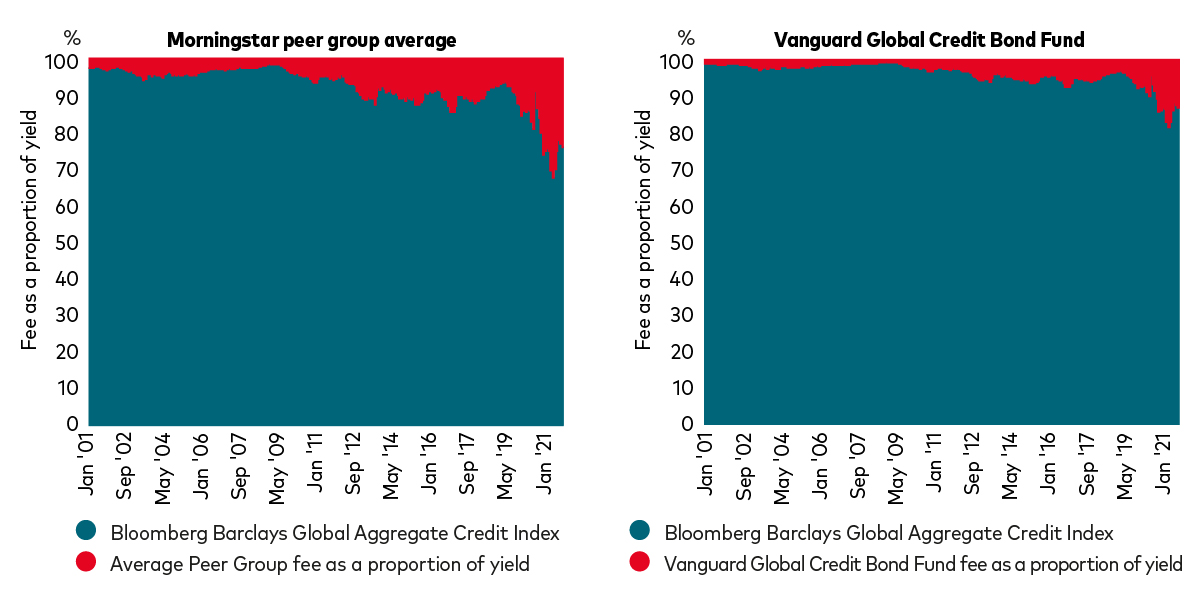

And as a fixed income pioneer, with more than $1.7tn in active fixed income assets globally and over 35 years’ experience managing active strategies, our scale keeps our costs competitive, and drives a highly attractive value proposition. For our managers, low costs mean they are not pressured into taking excessive or outsize positions in order to achieve performance over and above a high fee threshold. Instead, they are able to focus on high-conviction ideas.

Vanguard Global Credit Bond Fund fees as a proportion of yield versus peer group

Source: Morningstar, Bloomberg Barclays Global Aggregate Credit Index Yield to Worst and Vanguard from 31 January 2001 to 28 May 2021.

Ultimately, this helps us generate consistent performance. Ninety-two percent of Vanguard’s active bond funds have beaten their five-year Lipper peer-group averages, and 86% over 10 years3.

Consistency through risk-adjusted alpha

We believe that active fixed income should be a strategic part of an investor’s asset allocation. Alpha is important - but it’s risk-adjusted alpha that is pivotal to consistency. By deriving alpha from genuine security selection across diversified sources, without taking excessive top-down directional risk, investors can access more consistent alpha generation with less downside risk.

Vanguard’s active fixed income philosophy

- Our active fixed income line-up is focused on ‘true-to-label’ products.

- Our funds, on average, have a similar risk and asset-class profile to the assets they represent.

- Our managers strive to achieve consistent alpha generation over the market cycle.

- Our investment guidelines allow flexibility to add value while staying true to the character of the funds.

- Our scale keeps our costs competitive, resulting in a highly attractive value proposition.

Written in collaboration with Kunal Mehta, senior investment specialist, fixed income.

Find out more about active fixed income at Vanguard.

1 Source: Bloomberg, JP Morgan and Morningstar Direct as at 31 June 2021. Between 1 July 2001 and 30 June 2021, emerging market hard-currency bonds (as represented by the J.P. Morgan EMBI Global Diversified index) had a lower standard deviation of return and higher return than global equities (as represented by the MSCI ACWI index). All performance calculated in USD. Past performance is not a reliable indicator of future results.

2 Peer group defined by Morningstar - EAA OE Global Corporate Bond - USD Hedged.

3 Source: Lipper, a Thomson Reuters Company. Data as at 31st December 2020. The percentage of Vanguard funds globally in each category that outperformed the average return of their peer group of mutual funds. For the five-year period, 44 of 48 bond funds Vanguard funds outperformed their peer group averages. For the ten-year period, 38 of 44 bond funds Vanguard funds outperformed their peer group averages. Results will vary for other time periods. Only funds with a minimum five- or ten-year history, respectively, were included in the comparison.

Investment risk information

The value of investments, and the income from them, may fall or rise and investors may get back less than they invested.

Past performance is not a reliable indicator of future results.

Some funds invest in emerging markets which can be more volatile than more established markets. As a result the value of your investment may rise or fall.

Investments in smaller companies may be more volatile than investments in well-established blue chip companies.

Reference in this document to specific securities should not be construed as a recommendation to buy or sell these securities, but is included for the purposes of illustration only.

Funds investing in fixed interest securities carry the risk of default on repayment and erosion of the capital value of your investment and the level of income may fluctuate. Movements in interest rates are likely to affect the capital value of fixed interest securities. Corporate bonds may provide higher yields but as such may carry greater credit risk increasing the risk of default on repayment and erosion of the capital value of your investment. The level of income may fluctuate and movements in interest rates are likely to affect the capital value of bonds.

The Vanguard Emerging Markets Bond Fund may use derivatives, including for investment purposes, in order to reduce risk or cost and/or generate extra income or growth. For all other funds they will be used to reduce risk or cost and/or generate extra income or growth. The use of derivatives could increase or reduce exposure to underlying assets and result in greater fluctuations of the Funds net asset value. A derivative is a financial contract whose value is based on the value of a financial asset (such as a share, bond, or currency) or a market index.

The Vanguard Global Credit Bond Fund may use derivatives, including for investment purposes, in order to reduce risk or cost and/or generate extra income or growth. For all other funds they will be used to reduce risk or cost and/or generate extra income or growth. The use of derivatives could increase or reduce exposure to underlying assets and result in greater fluctuations of the Funds net asset value. A derivative is a financial contract whose value is based on the value of a financial asset (such as a share, bond, or currency) or a market index.

Some funds invest in securities which are denominated in different currencies. Movements in currency exchange rates can affect the return of investments.

For further information on risks please see the “Risk Factors” section of the prospectus on our website at https://global.vanguard.com.

Important information

This is an advertising document.

For professional investors only (as defined under the MiFID II Directive) investing for their own account (including management companies (fund of funds) and professional clients investing on behalf of their discretionary clients). In Switzerland for professional investors only. Not to be distributed to the public.

The information contained in this document is not to be regarded as an offer to buy or sell or the solicitation of any offer to buy or sell securities in any jurisdiction where such an offer or solicitation is against the law, or to anyone to whom it is unlawful to make such an offer or solicitation, or if the person making the offer or solicitation is not qualified to do so. The information in this document is general in nature and does not constitute legal, tax, or investment advice. Potential investors are urged to consult their professional advisers on the implications of making an investment in, holding or disposing of shares and /or units of, and the receipt of distribution from any investment.

Vanguard Investment Series plc has been authorised by the Central Bank of Ireland as a UCITS and has been registered for public distribution in certain EEA countries and the UK. Prospective investors are referred to the Funds' prospectus for further information. Prospective investors are also urged to consult their own professional advisers on the implications of making an investment in, and holding or disposing shares of the Funds and the receipt of distributions with respect to such shares under the law of the countries in which they are liable to taxation.

The Manager of Vanguard Investment Series plc is Vanguard Group (Ireland) Limited. Vanguard Asset Management, Limited is a distributor of Vanguard Investment Series plc.

For further information on the fund's investment policies, please refer to the Key Investor Information Document (“KIIDs”). The KIID for this fund is available in local languages, alongside the prospectus via Vanguard’s website https://global.vanguard.com/.

The funds or securities referred to herein are not sponsored, endorsed, or promoted by MSCI, and MSCI bears no liability with respect to any such funds or securities. The prospectus or the Statement of Additional Information contains a more detailed description of the limited relationship MSCI has with Vanguard and any related funds.

Information has been obtained from sources believed to be reliable but J.P. Morgan does not warrant its completeness or accuracy. The Index referenced herein is used with permission. The Index may not be copied, used, or distributed without J.P. Morgan’s prior written approval. Copyright 2016, J.P. Morgan Chase & Co. All rights reserved.

For Dutch investors only: The fund(s) referred to in this document are listed in the AFM register as defined in section 1:107 Dutch Financial Supervision Act (Wet op het financieel toezicht).For details of the Risk indicator for each fund listed in this document, please see the fact sheet(s) which are available from Vanguard via our website https://www.vanguard.nl/portal/instl/nl/en/product.html.

For Swiss professional investors: The Manager of Vanguard Investment Series plc is Vanguard Group (Ireland) Limited. Vanguard Investments Switzerland GmbH is a financial services provider, providing services in the form of purchase and sales according to Art. 3 (c)(1) FinSA. Vanguard Investments Switzerland GmbH will not perform any appropriateness or suitability assessment. Furthermore, Vanguard Investments Switzerland GmbH does not provide any services in the form of advice. Vanguard Investment Series plc has been authorised by the Central Bank of Ireland as a UCITS. Prospective investors are referred to the Funds' prospectus for further information. Prospective investors are also urged to consult their own professional advisors on the implications of making an investment in, and holding or disposing shares of the Funds and the receipt of distributions with respect to such shares under the law of the countries in which they are liable to taxation. Vanguard Investment Series plc has been approved for offer in Switzerland by the Swiss Financial Market Supervisory Authority (FINMA). The information provided herein does not constitute an offer of Vanguard Investment Series plc in Switzerland pursuant to FinSA and its implementing ordinance. This is solely an advertisement pursuant to FinSA and its implementing ordinance for Vanguard Investment Series plc. The Representative and the Paying Agent in Switzerland is BNP Paribas Securities Services, Paris, succursale de Zurich, Selnaustrasse 16, 8002 Zurich. Copies of the Articles of Incorporation, KIID, Prospectus, Declaration of Trust, By-Laws, Annual Report and Semiannual Report for these funds can be obtained free of charge from the Swiss Representative or from Vanguard Investments Switzerland GmbH via our website https://global.vanguard.com/.

Issued in EEA by Vanguard Group (Ireland) Limited which is regulated in Ireland by the Central Bank of Ireland.

Issued in Switzerland by Vanguard Investments Switzerland GmbH.

Issued by Vanguard Asset Management, Limited which is authorised and regulated in the UK by the Financial Conduct Authority.

© 2021 Vanguard Group (Ireland) Limited. All rights reserved.

© 2021 Vanguard Investments Switzerland GmbH. All rights reserved.

© 2021 Vanguard Asset Management, Limited. All rights reserved.